A big warning signal just flashed in our inbox recently.

As mortgage rates are rising at one of the fastest paces in history …

“Due to the extreme market volatility in the MBS market, effective immediately all locks will now be converted to 30 day locks commencing from the original rate lock date [even if you had a 60-day lock!] As long as the loan is able to close within 30 days of the original lock date, the loan will close at the currently locked rate. If the loan is not able to close before the lock expiration date, the loan will have to be relocked at the current market rate as of the date of expiration. The 30-day lock policy will be applicable to all loans in the pipeline. Since this loan has passed 30 days from the original lock date, you will need to relock the loan with current market rates starting on April 1, 2022. This is something we didn’t want to do, but must be done in order for us to keep funding.

This was obviously a very difficult decision that was forced by instability and volatility never before seen in such a short period of time in the MBS secondary market. Unfortunately pricing on the secondary market has increased with such velocity that we are simply unable to extend these locks past 30 days at their current rates. We are hoping this volatility comes to an end very soon so we can get back to normal business.”

– March 31, 2022 from an actual non-conforming lender

WOW. This is a reality check. And a reminder of the counterparty risk everywhere in our financial system.

Fortunately, after major backlash the lender agreed to honor the original locks and our clients did not lose their rates. But the scare drove some points home.

Point #1: Respect your rate lock expiration date!

Lock with plenty of time to close, rush your appraisals if needed, and support your lending team with supplying requested documents as quickly as possible. Our team is prepared to close in 14-21 days on purchases with conventional financing when we have a properly prepared financial package ready to go for you. Advance planning goes a long way in today’s competitive market.

To discuss getting in a strong buying position, schedule a Personal Strategy Session here.

Point #2: Lock ASAP.

Our lenders will lock as far out as 75-365 days (helpful for those of you in new construction contracts). If rates do take a turn for the better, you’ll likely have a float down option you can exercise.

Point #3: Don’t wait for rates to drop. Though, it’s likely eventually.

Mortgage rates rise and fall with inflation expectations. With real interest rates around -7% (Fed Funds Rate – CPI), do mortgage bond buyers really believe that hiking the Fed Funds Rate by a few percentage points is going to turn yields and inflation around? Could the Fed really be stepping out of the MBS market, not because they see strength, but because they’re getting out (of whatever they can!) before a debt market implosion (bond prices collapse / rates rise sharply)? Yes, the yield curve is flashing inversions and during recessions typically mortgage rates come down as recessions are deflationary in nature and the Fed typically pulls out all the stops to cushion the blow.

However, are we simply looking at inflation and deflation ebbs and flows or could there be a world of stagflation upon us where we continue to see high inflation while simultaneously seeing less and less economic growth … Ouch.

If an affordability crisis is picking up steam, fixing your housing expense for yourself (and/or to pass on to your tenants or future buyers) makes a lot of sense. If the Fed can rescue the mortgage bond market and keep rates palatable for the masses, it’ll come at a price that future generations will pay dearly for (think hyperinflation). In that case, make sure you’re on the winning side by owning real assets with fixed rate debt.

A final point to ponder …

If mortgage interest rates continue to spike drastically, will this cause a housing crash and a buying opportunity?

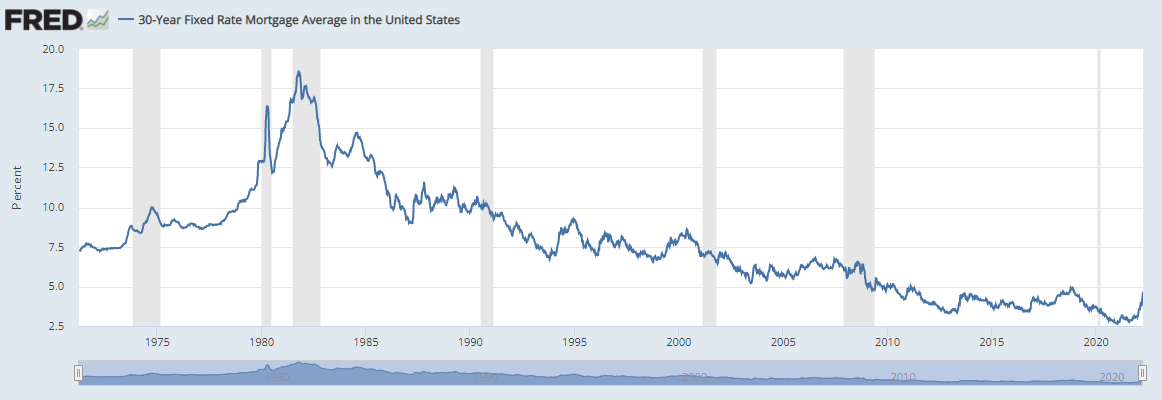

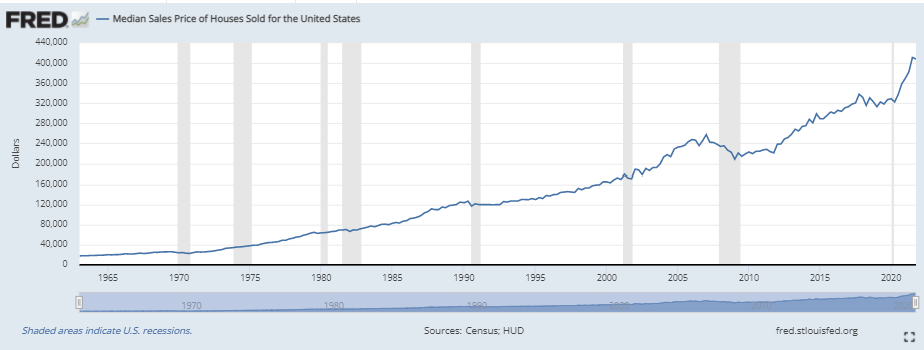

Looking back at history and comparing the below charts of historical trends in 30 year Fixed Mortgage Rates and the Median Sales Price of Homes in the U.S.…

We selected for analysis the biggest spikes in mortgage rates that we could find and charted the home prices around (or just following) that same time period.

Bottom Line: With rare exception, as mortgage rates rose …

SURPRISE! SO DID MEDIAN HOUSE PRICES!